Residential PV

Units using capacity above represent kWDC.

2022 ATB data for residential solar photovoltaics (PV) are shown above, with a Base Year of 2020. The Base Year estimates rely on modeled capital expenditures (CAPEX) and operation and maintenance (O&M) cost estimates benchmarked with industry and historical data. Capacity factor is estimated based on hours of sunlight at latitude for 10 resource categories in the United States, binned by mean global horizontal irradiance (GHI). The 2022 ATB presents capacity factor estimates that encompass a range associated with advanced, moderate, and conservative technology innovation scenarios across the United States. Future-year projections are derived from bottom-up benchmarking of PV CAPEX and bottom-up engineering analysis of O&M costs.

The three scenarios for technology innovation are:

- Conservative Technology Innovation Scenario (Conservative Scenario): lower levels of R&D investment with minimal technology advancement and global module pricing consistent with the base year

- Moderate Technology Innovation Scenario (Moderate Scenario): R&D investment continuing at similar levels as today, with no substantial innovations or new technologies introduced to the market

- Advanced Technology Innovation Scenario (Advanced Scenario): an increase in R&D spending that generates substantial innovation, allowing historical rates of development to continue.

Resource Categorization

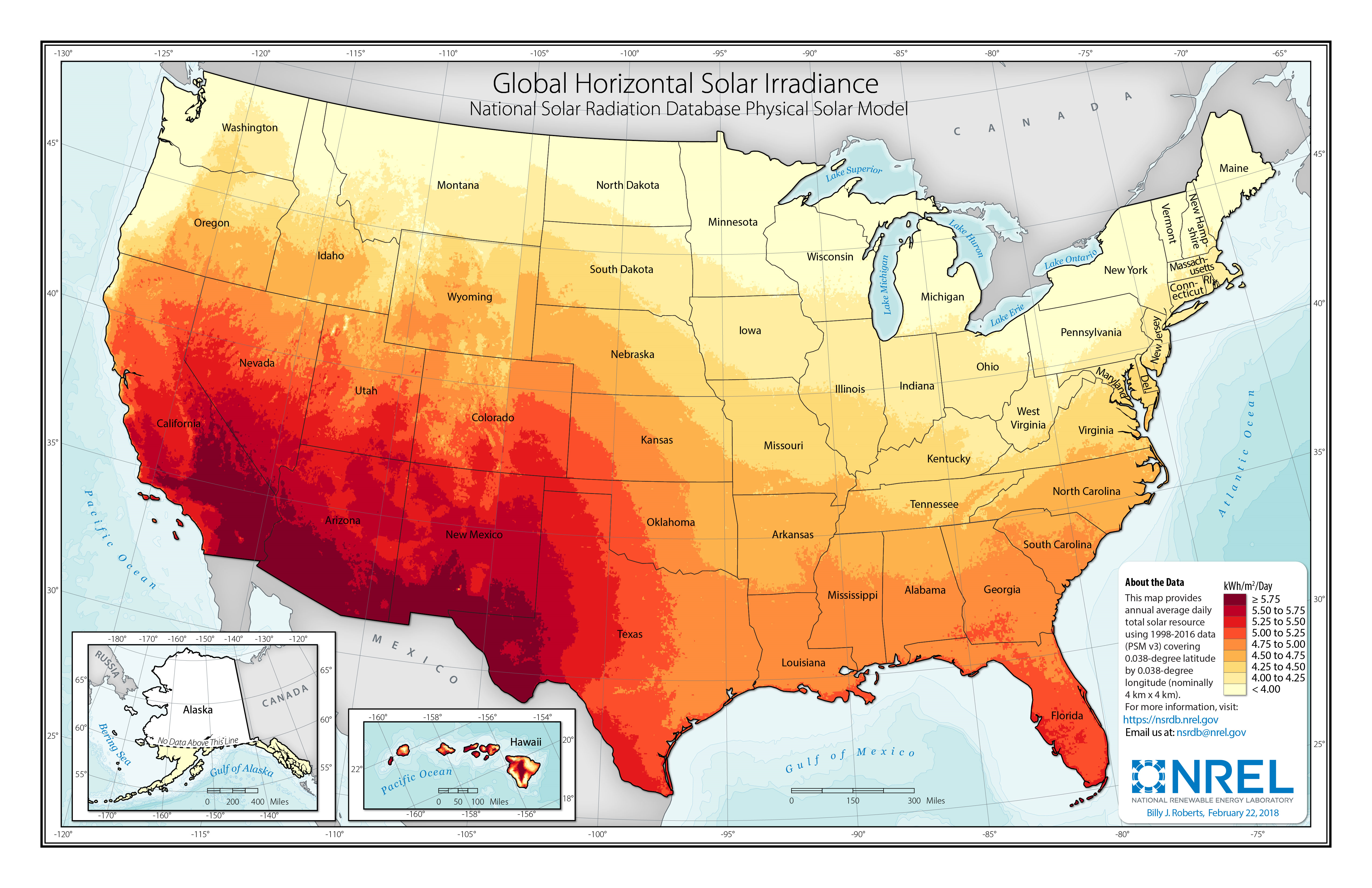

The ATB provides the average capacity factor for 10 resource categories in the United States, binned by mean GHI. The annual average capacity factor for the contiguous United States is calculated using the Renewable Energy Potential (ReV) model using solar resource data for 2012 from the National Solar Radiation Database (NSRDB). The county-level capacity factors are calculated for specific locations with azimuth and tilt, which are based on representative agents selected in the Distributed Generation Market Demand Model (dGen) 2020 Standard Scenarios agent database (Sigrin et al., 2016). A lookup table for these locations and the NSRDB is generated based on nearest distance. The azimuth and tilt as well as the resource GHI are used to generate a System Advisor Model (SAM) config file and to run reV, which outputs the annual average capacity factor at each evaluated location. The U.S. average capacity factor for each resource category is weighted by the population of each county within the GHI resource category. The county estimated populations are provided by geospatial and tabular data from the U.S. Census. The map below shows average annual GHI in the United States.

The following table summarizes estimated 2019 capacity factors (in the first year of operation) for each resource category and each resource category's associated population.

| Resource Class | GHI Bin (kWh/m2/day) | Mean DC Capacity Factor | Population |

| 1 | >5.75 | 19.6% | 12,554,678 |

| 2 | 5.5–5.75 | 19.3% | 21,403,290 |

| 3 | 5.25–5.5 | 18.0% | 13,476,871 |

| 4 | 5–5.25 | 17.0% | 30,603,630 |

| 5 | 4.75–5 | 16.1% | 45,176,116 |

| 6 | 4.5–4.75 | 15.9% | 39,880,837 |

| 7 | 4.25–4.5 | 15.2% | 31,742,606 |

| 8 | 4–4.25 | 14.5% | 80,155,804 |

| 9 | 3.75–4 | 13.9% | 40,755,023 |

| 10 | <3.75 | 12.7% | 10,255,830 |

| Mean | 15.7% |

DOE’s Solar Energy Technologies Office sets its PV cost targets for a location centered geographically within the contiguous United States, in Resource Class 7, whereas the ATB benchmark uses Class 5, representing the national-average solar resource.

Scenario Descriptions

| Scenario | Module Efficiency1 | Inverter and Power Electronics | Installation Efficiencies | Energy Yield Gain1 |

|---|---|---|---|---|

| Conservative Scenario | Technology Description: Tariffs expire as scheduled, though some form of trade friction still remains, keeping U.S. panel pricing halfway between base year U.S. pricing and global pricing. Efficiency gains for panels are consistent with one standard deviation below those of the International Technology Roadmap for Photovoltaic (ITRPV—an annual document prepared by many leading international poly-Si producers, wafer suppliers, c-Si solar cell manufacturers, module manufacturers, PV equipment suppliers, and production material providers, as well as PV research institutes and consultants) to 2030, which are well below the historical monofacial average gains and below the leveling-off point to 21.5% by 2030, resulting in a price of $0.32/WDC (Feldman et al., 2021). Justification: This scenario represents the low end of manufacturers' expectations and additional trade friction despite the scheduled removal of the tariff. | Technology Description: This scenario assumes a larger market size. Justification: The global PV industry is expected to continue to expand. | N/A | N/A |

| Moderate Scenario | Technology Description: Tariffs expire as scheduled, and efficiency gains are consistent with median ITRPV values to 2030, which are well below historical monofacial average gains and below the leveling-off point (22.5%), resulting in a price of $0.19/WDC. Justification: This scenario represents manufacturers' expectations for 2030. | Technology Description: This scenario assumes design simplification and manufacturing automation. Justification: Industry is transitioning toward greater simplification and automation. | Technology Description: This scenario assumes 20% labor and hardware balance-of-system (BOS) cost improvements through automation, preassembly of racking, mounting, and wiring efficiencies, and improvements in wind load design. It also assumes a switch in deployments to be a standard feature of the construction of a house or a normally scheduled reroofing event. Justification: Because residential PV systems represent a smaller investment in absolute dollars, soft costs—such as customer acquisition, permitting, interconnection, and overhead—contribute a significantly higher percentage of CAPEX than they do with larger PV systems. Incorporating the PV system into a larger related construction project, such as a reroofing or the construction of a new house, could create significant efficiencies to customer acquisition costs and to permitting, inspection, and interconnection costs, as well as reduced costs through efficiencies in labor and structural BOS. (Feldman et al., 2021) found that PV systems in new homes were 24% less expensive than retrofit residential PV systems. | Technology Description: This scenario assumes a 2% energy gain and a degradation rate reduction from 0.7%/yr to 0.5%/yr. Justification: Significant R&D is currently spent on improved cell temperatures and lower degradation rates. Degradation rates of 0.5%/yr are already common for some developers. |

| Advanced Scenario | Technology Description: Modules maintain the historical average of 0.5% absolute efficiency improvement per year to reach 25% in 2030, which results in a price of $0.17/WDC. Justification: Manufacturers reported mass-produced cell efficiencies will increase from 20%–23% in 2018 to 21%–24% by 2021. Mass-production monocrystalline and silicon heterojunction technologies have already achieved cell efficiency records in a laboratory of 26.1% and 26.7%, respectively.

| Technology Description: This scenario assumes design simplification and manufacturing automation. Justification: The power electronics industry already has road maps to simplify and automate current products, and there is more potential with increased industry size. | Technology Description: This scenario assumes 20% labor and hardware BOS cost improvements through automation and preassembly of racking, mounting, and wiring efficiencies. It also assumes a switch in deployments to be a standard feature of the construction of a house or a normally scheduled reroofing event (e.g., new construction or reroofing). Justification: In addition to the justifications listed above, there is potential for a national streamlined permitting process, with efforts currently underway. For example, the Solar Automated Permit Processing platform (SolarAPP+) is being designed to be an instant online solar permitting tool for code-compliant residential systems. | Technology Description: This scenario assumes a 4% energy gain and a degradation rate reduction from 0.7%/yr to 0.2%/yr. Justification: Significant R&D is currently spent on improved cell temperatures and lower degradation rates. Degradation rates of 0.2%/yr are currently being pursued. |

| Impacts |

|

|

|

|

| References |

1 Module efficiency improvements represent an increase in energy production over the same area, in this case the dimensions of a PV module. Energy yield gain represents an improvement in capacity factor relative to the rated capacity of a PV system.

Representative Technology

For the 2022 ATB, residential PV systems are modeled for a 7.15-kWDC, fixed tilt, roof-mounted system with a 1.15 DC-to-AC ratio, or inverter loading ratio (ILR) (Ramasamy et al., 2021). Flat-plate PV can utilize direct and indirect insolation, so PV modules need not directly face and track incident radiation. The county-level capacity factors are calculated for specific locations, which are based on representative agents selected in the dGen 2020 Standard Scenarios agent database (Sigrin et al., 2016). At each location, various tilt/azimuth combinations were evaluated, and the optimal combination was chosen for modeling. The ability to use direct and indirect insolation gives rooftop PV systems a broad geographical application.

Methodology

This section describes the methodology to develop assumptions for CAPEX, O&M, and capacity factor. For standardized assumptions, see regional cost variation, materials cost index, scale of industry, policies and regulations, and inflation. The PV-specific and standardized assumptions for labor cost differ; the PV analysis assumes use of nonunion labor only.

Currently, CAPEX—not levelized cost of energy (LCOE)—is the most common metric for PV cost. Because of different assumptions in long-term incentives, system location and production characteristics, and cost of capital, LCOE can be confusing and often incomparable for different estimates. Though CAPEX also has many assumptions and interpretations, it involves fewer variables to manage. Therefore, PV projections in the 2022 ATB are driven entirely by plant and operational cost improvements.

Three projections are developed for scenario modeling as bounding levels (see the scenario list above).

Capital Expenditures (CAPEX)

Definition: Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. For residential PV, this is modeled for only a host-owned business model.

For the 2022 ATB—and (EIA, 2016) and the National Laboratory of the Rockies (NLR) PV cost model—the residential PV plant envelope is defined to include items noted in the table (Components of CAPEX) below.

Base Year: Reported residential PV installation CAPEX (Barbose et al., 2021) is shown (see chart below) in box-and-whiskers format for comparison to historical residential PV benchmark overnight capital cost and the 2022 ATB estimates of future CAPEX projections. The data in (Barbose et al., 2021) represent 79% of all U.S. residential PV and commercial PV capacity installed through 2020.

Historical Sources: (Barbose et al., 2021); (Ramasamy et al., 2021)

Future Projections: 2022 ATB

Reported and benchmark prices can differ for a variety of reasons, as outlined by Barbose and Darghouth (Barbose et al., 2019) and Bolinger, Seel, and Robson (Bolinger et al., 2019), including:

- Timing-related issues (e.g., the time between contract completion and project placement in service may vary)

- Variations over time in the size, technology, installer margin, and design of systems installed in a given year

- Which cost categories are included in CAPEX (e.g., financing costs and initial O&M expenses).

Federal investment tax credits provide an incentive to include costs in the upfront CAPEX to receive a higher tax credit, and these included costs may have otherwise been reported as operating costs. The bottom-up benchmarks are more reflective of an overnight capital cost, which is in line with the ATB methodology of inputting overnight capital cost and calculating construction financing to derive CAPEX.

Residential PV pricing and capacities are quoted in kWDC (i.e., module rated capacity) unlike other generation technologies (including utility-scale PV), which are quoted in kWAC. This is because kWDC is the unit that most of the residential PV industry uses. Although costs are reported in kWDC, the total CAPEX includes the cost of the inverter, which has a capacity measured in kWAC.

CAPEX estimates for 2021 reflect a continued rapid decline in pricing supported by analysis of recent system cost and pricing for projects that became operational in 2021 (Ramasamy et al., 2021). Although the PV technologies vary, typical installation costs are represented with a single estimate per innovation scenario, because residential PV CAPEX does not correlate well with solar resource. Although the technology market share may shift over time with new developments, the typical installation cost is represented with the projections above.

System prices of $2.74/WDC in 2020 and $2.65/WDC in 2021 are based on bottom-up benchmark analysis reported in U.S. Solar Photovoltaic System and Energy Storage Cost Benchmarks: Q1 2021 (Ramasamy et al., 2021).

The Base Year CAPEX estimates should tend toward the low end of observed cost, because no regional impacts are included. These effects are represented in the historical market data.

Future Years:

Projections of 2030 residential PV plant CAPEX are based on bottom-up cost modeling, with 2021 values from (Ramasamy et al., 2021) and a straight-line change in price in the intermediate years between 2021 and 2030. The system design and price changes made in the models are summarized and described in the Summary of Technology Innovations by Scenario table. See Cost Details by Scenario below for the details of changes to components of system price in the different ATB scenarios.

We assume each scenario's 2050 CAPEX is the equivalent of the 2030 CAPEX of the scenario but one degree more aggressive, with a straight-line change in price in the intermediate years between 2030 and 2050. In the table below, asterisks and daggers indicate corresponding cells, where scenarios use the same values but are shifted in time. We also develop and model a scenario one degree more aggressive than the Advanced Scenario to estimate its 2050 CAPEX. The 2050 Advanced Scenario assumes a module efficiency of 30%; further inverter simplification and manufacturing automation; 35% labor and hardware BOS cost improvements through automation and preassembly of racking, mounting, and wiring; replacement of steel and aluminum with carbon fiber, which cuts material costs in half; and that PV systems become a standard feature of the construction of a house or during a normally scheduled reroofing event (i.e., new construction/reroof).

| Year | Advanced Scenario (Increased R&D) | Moderate Scenario (Current R&D) | Conservative Scenario (Decreased R&D) |

|---|---|---|---|

| 2030 | *Residential PV CAPEX: $0.79/WDC | † Residential PV CAPEX: $1.02/WDC | Residential CAPEX: $2.29/WDC |

| 2050 | $0.55/WDC | *$0.79/WDC | † $1.02/WDC |

More aggressive scenarios reach given CAPEX sooner, as indicated by the asterisks and daggers.

We compare the CAPEX scenarios over time to four analyst projections, adjusted for inflation. The median of those projections is displayed in the figure below through 2030. The 2022 ATB CAPEX projections are in line with the other projections through 2030. Two of the four analyst projections do not go beyond 2030, so data points with which to compare the ATB projections are limited; however, the Advanced Scenario is in line with the minimum analyst projection in 2050.

Sources: 2022 ATB; (BNEF, 2019); (BNEF, 2021); (Cox, 2021); (EIA, 2021)

Use the following table to view the components of CAPEX.

Operation and Maintenance (O&M) Costs

Definition: Operation and maintenance (O&M) costs represent the annual expenditures required to operate and maintain a PV plant over its lifetime, including items noted in the table below.

Base Year: Fixed O&M (FOM) of $29/kWDC-yr is based on modeled pricing for a residential PV system quoted in Q1 2020 as reported by (Feldman et al., 2021). Lawrence Berkeley National Laboratory collected feedback from U.S. solar industry professionals (Wiser et al., 2020). The wide range in reported prices depends in part on the maintenance practices that exist for a particular system. These cost categories include asset management (including compliance and reporting for incentive payments), insurance products, cleaning, vegetation removal, and component failure. Not all these practices are performed for each system; also, some factors depend on the quality of the parts and construction. NLR analysts estimate O&M costs can range from $0 to $40/kWDC-yr.

Future Years: FOM of $29/kWDC-yr for 2021 is based on pricing reported by (Ramasamy et al., 2021), which can be divided into system-related expenses ($25/kWDC-yr) and administration-related expenses ($4/kWDC-yr). From 2022 to 2050, FOM is based on the ratio of O&M costs ($/kW-yr) to CAPEX costs ($/kW), which was 1.0:100 in 2021 as reported by (Ramasamy et al., 2021). Historical data suggest O&M and CAPEX cost reductions are correlated; from 2010 to 2020, benchmark residential PV O&M fell 49% and PV CAPEX fell 64%, as reported by (Feldman et al., 2021). Administrative expenses are kept constant.

Use the following table to view the components of O&M.

Capacity Factor

Definition: The capacity factor represents the expected annual average energy production divided by the annual energy production assuming the plant operates at rated capacity for every hour of the year. It is intended to represent a long-term average over the lifetime of the plant; it does not represent interannual variation in energy production. Future-year estimates represent the estimated annual average capacity factor over the technical lifetime of a new plant installed in a given year.

Residential PV system capacity factor is not directly comparable to other technologies' capacity factors. Other technologies' capacity factors (including utility-scale PV) are represented exclusively in AC units (see Solar PV AC-DC Translation). However, because residential PV pricing in the 2022 ATB is represented in $/WDC, residential PV system capacity is a DC rating. Because each technology uses consistent capacity ratings, the LCOEs are comparable.

The capacity factor is influenced by the hourly solar profile, technology (e.g., thin-film or crystalline silicon), expected downtime, and inverter losses to transform from DC to AC power. The DC-to-AC ratio is a design choice that influences the capacity factor.

PV plant capacity factor incorporates an assumed degradation rate of 0.7%/yr (Feldman et al., 2021) in the annual average calculation.

R&D could lower degradation rates of PV plant capacity factor; future projections for the Moderate Scenario and the Advanced Scenario reduce degradation rates by 2030, using a straight-line basis, to 0.5%/yr, and 0.2%/yr respectively. The Conservative Scenario assumes no improvement in degradation rates through 2030.

Base Year: In the interactive data chart at the top of this page, select Technology Detail = All to add filters to the initial figure showing a range of capacity factors based on variation in solar resource in the contiguous United States. The ATB provides the average capacity factor for 10 resource categories in the United States, binned by mean GHI. The annual average capacity factor for the contiguous United States is calculated using the reV model using solar resource data for 2012 from the NSRDB. The county-level capacity factors are calculated for specific locations with azimuth and tilt, which are based on representative agents selected in the dGen 2020 Standard Scenarios agent database (Sigrin et al., 2016). A lookup table for these locations and the NSRDB is generated based on nearest distance. The azimuth and tilt as well as the resource GHI are used to generate a System Advisor Model (SAM) config file and to run reV, which outputs the annual average capacity factor at each evaluated location. U.S. average capacity factor for each resource category is weighted by the population of each county within the GHI resource category. The county estimated populations are provided by geospatial and tabular data from the U.S. Census.

First-year operation capacity factors as modeled range from 12.7% for Class 10 (for locations with an average annual GHI less than 3.75) to 19.6% for Class 1 (for locations with an average annual GHI greater than 5.75). Actual systems will vary significantly depending on location and system configuration (e.g., south-facing or west-facing).

Over time, PV installation output is reduced because of degradation in module quality, which is accounted for in ATB estimates of capacity factor over the 30-year lifetime of the plant. The adjusted average capacity factor values in the 2020 ATB Base Year range from 12.0% for Class 10 (for locations with an average annual GHI less than 3.75) to 18.5% for Class 1 (for locations with an average annual GHI greater than 5.75).

Future Years: Projections of capacity factors for plants installed in future years increase over time because of reduced system losses, and a straight-line reduction in PV plant capacity degradation rates from 0.7%/yr that reach 0.5%/yr and 0.2%/yr by 2030 for the Moderate Scenario and the Advanced Scenario respectively. The Conservative Scenario assumes no improvement in degradation rates through 2030. The following table summarizes the difference in average capacity factor in 2030 caused by these changes in the technology innovation scenarios. Similar to our CAPEX assumptions, we assume each scenario's 2050 capacity factor is the equivalent of the 2030 capacity factor of the scenario but one degree more aggressive, with a straight-line change in price in the intermediate years between 2030 and 2050.

| Scenario | Average Capacity Factor in 2030 (Class 10 - Class 1) | Percentage Improvement from Base Year (2020) |

|---|---|---|

| Advanced Scenario (0.20%/yr degradation rate) | 12.5%–19.3% | 4.3% |

| Moderate Scenario (0.50%/yr degradation rate) | 12.2%–18.8% | 1.7% |

| Conservative Scenario (0.7%/yr degradation rate) | 12.0%–18.5% | 0% |

PV plants have very little downtime, and inverter efficiency is already optimized. Even so, there is potential for future increases in capacity factors through technological improvements beyond lower degradation rates, such as less panel reflectivity and improved performance in low-light conditions.

References

The following references are specific to this page; for all references in this ATB, see References.